Intern Breakdown #1: GBTC

The Grayscale Bitcoin Trust explained at 3 levels of depth (👶, 🐸, 🧠)

The Grayscale Bitcoin Trust (GBTC) is a hot topic right now. On the surface, it’s a fairly straightforward entity — it’s a fund that literally just holds bitcoin — but it’s also contributed to some of the largest blowups in crypto history. Risky, leveraged GBTC trades made by firms like Three Arrows Capital are proving to be the spark that’s ignited a variety of problems across the industry, affecting lenders, brokerages, and traders alike.

This breakdown looks to demystify GBTC by examining it at 3 levels of depth so that you’ll learn something whether you’re a crypto newbie or SBF himself. Maybe it’ll even help you understand the tidal wave of acronyms you’re seeing on Twitter (WTF is GBTC? Unfortunately for 3AC, it’s not BTC, it doesn’t trade at NAV, and it’s not an ETF thanks to the SEC lol.)

Level 1: Normie

Buying crypto can be a hassle. It’s even worse for big institutions that aren’t crypto-native and have to consider all sorts of complex laws and tax policies when making investments.

GBTC allows investors to get exposure to bitcoin without having to buy/hold/manage the actual coins themselves. Owning GBTC shares instead of raw BTC eliminates risks and inconveniences such as:

Purchasing and setting up a hardware wallet

Storing the seed phrase somewhere safe

Making sure you don’t get hacked

How does the trust work? There’s a company (Grayscale) that owns a bunch of bitcoin in a fund, and investors can buy shares in this fund that are traded on the public stock market. Since the fund only does one thing — buys bitcoin — the value of these shares is derived entirely from the value of BTC.

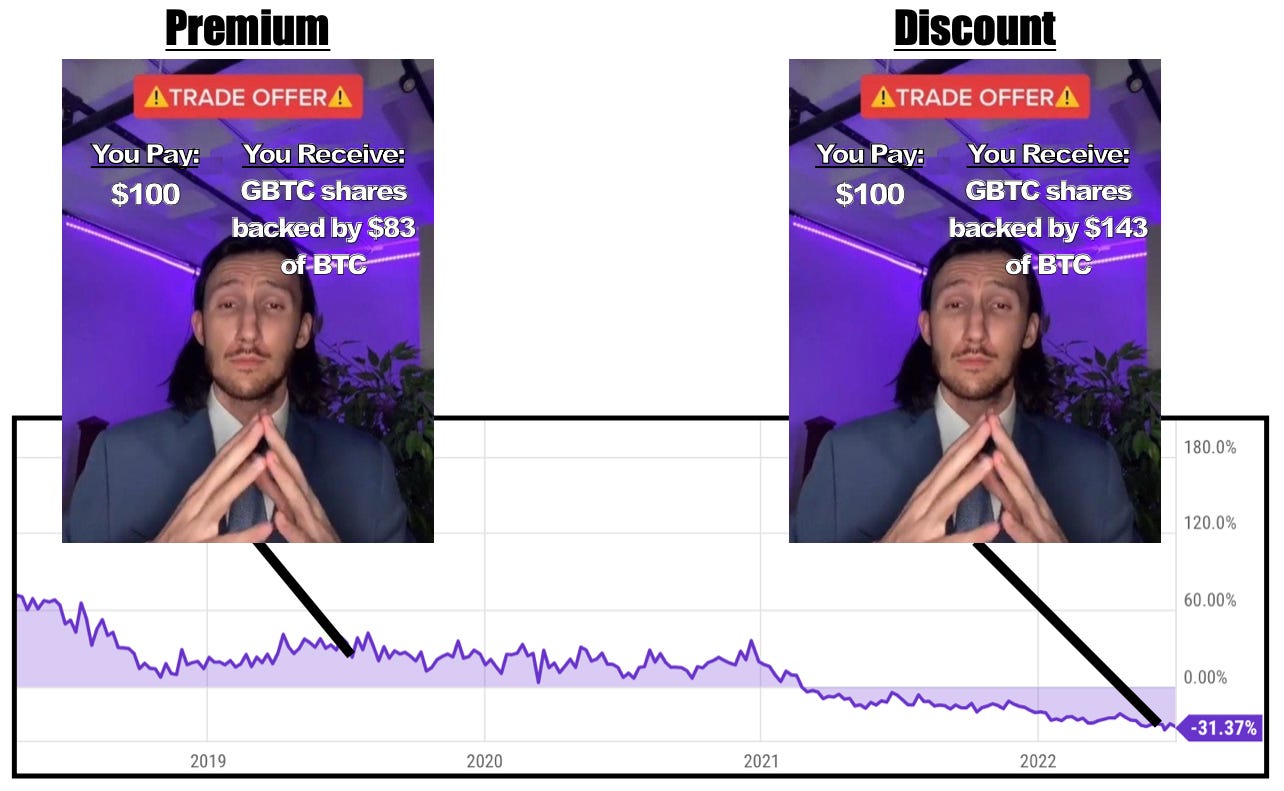

But this doesn’t mean the price of GBTC perfectly mirrors the price of BTC. Shares used to trade at a price above their underlying value — what’s called the net asset value (NAV) — until mid-2021. Then this premium flipped and became a discount, and for the past year, GBTC shares have traded well below the NAV.

Why would GBTC ever trade at a premium?

Reread the first sentence of this section — buying crypto can be a hassle. When the market was hot, institutions were willing to pay a premium to get exposure to crypto however they legally could. GBTC used to be one of the only options that traded on the stock market, and it saved institutions the headache of managing their own coins. There are also tax advantages for trading GBTC rather than bitcoin itself, like the fact that certain accounts (e.g. IRA, Roth IRA) don’t provide tax breaks for bitcoin investments but do for publicly traded trusts.

Why would GBTC ever trade at a discount?

Unlike shares of an ETF, which investors can redeem for the value of the underlying assets, GBTC shareholders can’t exchange their shares for bitcoin. This means GBTC’s price is fundamentally driven by supply and demand for shares, which can be affected by more than just the price of the underlying coins.

For example, although GBTC was one of the earliest options for institutional investors to easily get exposure to crypto, it’s no longer the only game in town. Competing trusts such as the Osprey Bitcoin Trust offer lower management fees — 0.49% compared to Grayscale’s 2% — and investors moving to these cheaper options creates sell pressure for GBTC.

Level 2: Degen

GBTC is technically a “grantor trust” — a legal designation that means it acts like a closed-end fund. Importantly, shares in closed-end funds can’t easily be created or removed from the market. Since the price of GBTC is based on supply and demand for shares, this inflexibility is the reason why GBTC doesn’t trade at the NAV.

ETFs, on the other hand, use a creation/redemption mechanism (basically the OG mint/burn mechanism) that allows shares to be exchanged for the fund’s underlying assets and vice versa. If shares ever traded at a steep discount or premium to the NAV there would be an arbitrage opportunity, and traders would redeem or create shares until the prices fell back in line. It’s a bit like LUNA/UST, except not a Ponzi.

While ETFs offer the constant possibility for an arb trade whenever share price diverges from the NAV, GBTC once presented an arbitrage opportunity of its own. But The GBTC Trade was much riskier. It only worked when shares traded at a premium because although GBTC allows accredited investors to create shares, it doesn’t (currently) have a redemption mechanism to turn those shares back into bitcoin. Two important things to note about the creation process:

When accredited investors give bitcoin to Grayscale, they are issued newly created GBTC shares at NAV. So when GBTC was trading at a premium, they could buy new shares below market price through these private placements.

However, the investors must hold these shares for at least 6 months before selling them on the open market.

With that in mind, here’s (one version of) how The GBTC Trade works.

Borrow BTC

Purchase new shares of GBTC at NAV

Wait 6 months

Sell GBTC on the market for a premium

Pay back the borrowed BTC

Profit.

That’s all well and good until you decide to ape into an especially large trade with lots of leverage in, say, January 2021 when the GBTC premium was 17%. Six months later, it’s July and the premium has flipped to a discount of -14%. Uh oh.

This exact mistake was one of the first dominoes that led to 3AC’s insolvency. The firm was one of the largest holders of GBTC, and some people speculate that when the premium turned to a discount, they became increasingly desperate to find a way to make up for their losses. Their investments in LUNA and stETH certainly didn’t help. More on that in these notes:

We’re now seeing 3AC’s bad trade, and the fraud that followed, turn into a contagion that’s affecting the entire crypto market. Centralized lending firms like BlockFi that provided the BTC to leveraged traders in step 1 of The GBTC Trade are facing the repercussions of their poor risk management.

So what happens now? There are still a lot of normal, solvent GBTC holders looking at the charts and thinking either (a) this discount is a great buying opportunity or (b) this sucks, the discount only seems to be growing.

The only way for GBTC’s price to converge back to NAV is if there’s suddenly a spike in demand for GBTC shares (unlikely) or if Grayscale figures out a way to offer a mechanism for shares to be redeemed for the underlying bitcoin. Everyone’s asking: can the Grayscale devs suits do something???

They’re trying. Grayscale’s been committed to converting the trust into a spot ETF for a long time, which would allow shares to be freely exchanged for bitcoin. This redemption mechanism would close the discount as shareholders swapped GBTC for BTC until the price approached the NAV. Unfortunately, the SEC recently denied Grayscale’s most recent application to convert the trust to a spot ETF, after having struck down over a dozen other applications in the past year. Grayscale immediately responded to the ruling by announcing it would sue the SEC.

The tl:dr of the dispute is:

SEC: There aren’t enough investor protections. Bitcoin is plagued by market manipulation and fraud, and we don’t think it’s safe for people to put their money into a spot ETF.

Grayscale: Then why have you approved other bitcoin-based ETFs, like those based on futures and even one that lets investors short bitcoin? This decision is super arbitrary, and the vast majority of investors want this conversion to happen.

It’ll be interesting to see how Grayscale’s lawsuit develops, but don’t hold your breath for a quick resolution. In the meantime, a few possible developments could occur that might impact GBTC…

Level 3: Gigabrain

Before going any further, it’s worth addressing an idea many smart people have had to unlock the trust’s BTC for shareholders:

Grayscale seems to have seen this coming, though, and they’ve made sure their corporate bylaws address the possibility of a tender offer or activist takeover.

Grayscale, for its part, has taken other steps to try to reduce the discount — most notably a series of share repurchase agreements from its parent company, Digital Currency Group. It’s debatable just how effective they’ll be, though, with some calling the move a “slight of hand.”

Things look pretty bleak… is there any hopium to sustain GBTC shareholders?

Yes, but it’s an option Grayscale doesn’t like. The firm could decide to implement a “Reg M” redemption program, which would allow shares to be exchanged for bitcoin. Grayscale used to offer this redemption option until 2016 when they were forced to stop by — who else — the SEC 🤦♂️. The previous two sections oversimplified in saying that GBTC allows shares to be created but not redeemed (acting as a bitcoin “Hotel California”); Reg M makes redemptions possible, but what got Grayscale in trouble with the SEC is that a trust can’t offer Reg M redemptions at the same time it’s allowing investors to create new shares.

Now, though, Grayscale has halted inflows to the trust (not that anyone would want to trade in BTC for shares that are locked up for 6 months and then worth less than the coins were). So it could, in theory, restart a Reg M redemption program. Unfortunately for GBTC holders, Grayscale has made it clear that it’s deadset on pursuing ETF approval from the SEC as the only path toward redemptions. To understand why, consider the final variable in this complicated GBTC equation:

The GBTC Principal-Agent Problem:

Every year, Grayscale earns 2% on the assets in its trust. That’s 2% of the NAV, not 2% of the discounted GBTC shares, and it comes out to hundreds of millions of dollars in fees.

There’s no doubt a Reg M redemption program would benefit Grayscale’s investors. GBTC holders would see their shares jump as the discount closed. But what would happen to Grayscale? As investors raced to redeem their shares for bitcoin, assets would flood out of their trust. AUM would plummet. And every bitcoin that left would be one less bitcoin for the company to milk for a fee.

Grayscale would have to (a.) sharply cut its fee, (b.) accept much lower AUM, or (c.) both. We’re left with what Ryan Selkis calls the “The Grayscale-Gensler Stalemate” which benefits the SEC (they get to keep punting on ETF approval) and Grayscale (they get to paint the SEC as the bad guy even though they profit every day GBTC remains a bitcoin black hole) while burdening investors with $6b of capital impairment as a result of the discount.

Just because Grayscale and DCG stand to lose in the short term if a spot ETF gets approved doesn’t mean they aren’t sincerely trying to make it happen. They are, after all, suing the SEC, and their website is upfront about the fact that their products “have not met their investment objective.” But that’s the trouble with misaligned incentives and asymmetric information between a principal and an agent. Investors can’t be entirely sure that Grayscale is acting in their best interest, and if the discount keeps widening, you can count on shareholders pushing for Reg M.

Aaaand that’s a wrap for this first Intern Breakdown on GBTC. Will the discount widen? Will it close? Will Grayscale pursue Reg M redemptions? Will Grayscale v. SEC be the next Depp v. Heard? Only time will tell.